Under the new scheme, for which applications started on 09/01/2023 and will last until 10/04/2023, investment plans of all categories are included, except for those falling under the previous three categories of the New Development Law.

Eligible Activity Codes belong to the following groups:

"Entrepreneurship 360°" aims to complement the other Aid Schemes of the Development Law, as it targets investment plans concerning significant sectors for the national economy, which do not fall under other special categories. It is noted that investment plans of all categories are included, except those falling under the aid schemes for agri-food – primary production and processing of agricultural products – fisheries, manufacturing – supply chain, tourism investment support, and alternative forms of tourism.

Beneficiaries of the aid schemes of the Development Law, are investment entities established or having a branch in the Greek Territory at the time of commencement of the investment plan's operations and having one of the following forms:

a. Commercial company,

b. Cooperative,

c. Social Cooperative Enterprises (Koin.S.Ep.), Agricultural Cooperatives (AS), Producer Groups (Om.P.), Producer Organizations (OP), Urban Cooperatives, Agricultural Corporate Partnerships (A.E.S.),

d. Consortia conducting commercial activities,

e. Public and municipal enterprises and their subsidiaries, provided that:

– they have not been assigned to serve a public purpose,

– the provision of services has not been exclusively assigned to them by the state,

– their operation is not subsidized by public resources during the period of long-term obligations defined by Law 4887/22 (articles 22 & 25).

a. Creation of a new unit.

b. Expansion of the capacity of an existing unit.

c. Diversification of a unit's production into products or services never previously produced or provided, with the condition that for large enterprises, the eligible expenses exceed at least 200% of the accounting value of the assets used again, as recorded in the tax year preceding the application for inclusion of the investment plan.

d. Fundamental change of the entire production process of an existing unit.

Eligible Expenses for Regional Aid – Categories of Expenses:

a. Building Facilities. Expenses for the construction, expansion, and modernization of building facilities, including special and auxiliary installations, as well as building constructions ensuring accessibility for people with disabilities.

b. Outdoor Area Works. Earthworks, Landscaping, Fencing, Biological Treatment Facilities, Planting, Outdoor Electrical Installations, Outdoor Plumbing, Water Supply.

c. Machinery – Technical – Special Installations. Purchase and installation of modern machinery, including technical installations and general arrangements for their permanent installation and connection to the production cycle. Expenses for the construction, purchase, supply, or modernization of special installations (e.g., heating systems, air conditioning units, or storage tanks).

d. Other equipment. Expenses for the purchase and installation of other equipment or/and office furniture and utensils only if they are a basic part of the investment's productive equipment.

e. Transport Means. Any vehicles used by the company for the transportation of personnel and customers, provided that they move within the unit's premises. Vehicles with up to 6 seats are not eligible.

f. Purchase of fixed assets of a unit that ceased operation at least two years before the application submission date,

– Purchase of the unit's property (building)

– Purchase of the unit's machinery and other equipment

g. Intangible assets. Expenses for technology transfer – know-how, Product Certification, and Quality Assurance Procedures, Purchase and development of software, Business Organization Systems.

h. Payroll costs for new jobs.

The eligible expense is the payroll cost of the new jobs created as a result of the implementation of the investment plan, calculated for a period of two (2) years from the creation of each position.

Eligible Expenses Outside Regional Aid:

Aid amounts per enterprise size:

– The total aid amount per investment plan submitted by very small and small enterprises cannot exceed €3 million for all types of aid.

– The total aid amount per investment plan submitted by medium and large enterprises cannot exceed:

– €3 million for financial leasing subsidy or the subsidy of the cost of new employment creation, as well as grants in the case of aid for medium-sized enterprises in the Regional Units of Thrace.

– €5 million for tax exemption aid.

The total aid provided to each investment plan holder, including aid to associated or linked enterprises, cannot exceed a cumulative total of €20,000,000 for a single enterprise and €30,000,000 for all associated or linked enterprises.

The maximum percentage of state aid per Region and enterprise size is as follows:

| Region | Small | Medium | Large |

|---|---|---|---|

| North Aegean | 75% | 70% | 60% |

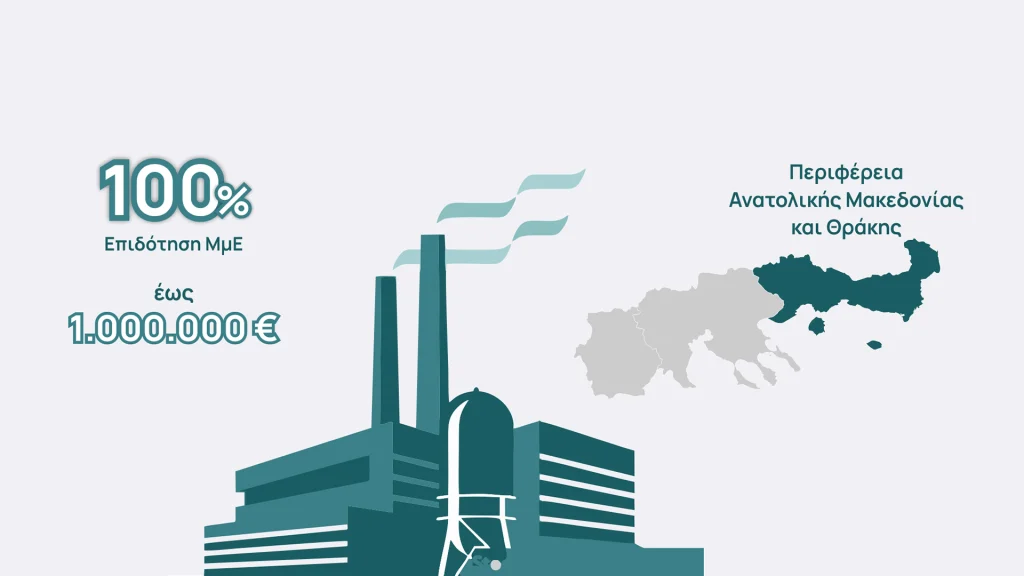

| Ανατολική Μακεδονία & Θράκη Central Macedonia Western Macedonia Epirus Thessaly Western Greece Crete Δήμοι Μεγαλούπολης, Τρίπολης, Γορτυνίας, Οιχαλίας | 70% | 60% | 50% |

| South Aegean Ionian Islands Central Greece Πελοπόννησος | 60% | 50% | 40% |

| Attica/Eastern-Western Attica/Piraeus/Islands | 45% | 35% | 25% |

| Western Sector of Attica | 35% | 25% | 15% |

For investment expenses in tangible fixed assets specifically for the construction, expansion, and modernization of buildings, the coefficient is set at 45%. This coefficient is set at eighty percent (80%) for investment plans implemented in buildings classified as preserved. For investment expenses in intangible assets, the coefficient is set at 50% for SMEs and 30% for large enterprises. Finally, for expenses concerning consultancy services, the coefficient is set at 50% for SMEs with a maximum limit of €50,000.

For more information, request a telephone appointment by clicking the button below, and a specialized economist from our company will contact you.

ΙΩΝΙΚΗ Finance

Under the new scheme, for which applications started on 09/01/2023 and will last until 10/04/2023, investment plans of all categories are included, except for those falling under the previous three categories of the New Development Law.

Eligible Activity Codes belong to the following groups:

"Entrepreneurship 360°" aims to complement the other Aid Schemes of the Development Law, as it targets investment plans concerning significant sectors for the national economy, which do not fall under other special categories. It is noted that investment plans of all categories are included, except those falling under the aid schemes for agri-food – primary production and processing of agricultural products – fisheries, manufacturing – supply chain, tourism investment support, and alternative forms of tourism.

Beneficiaries of the aid schemes of the Development Law, are investment entities established or having a branch in the Greek Territory at the time of commencement of the investment plan's operations and having one of the following forms:

a. Commercial company,

b. Cooperative,

c. Social Cooperative Enterprises (Koin.S.Ep.), Agricultural Cooperatives (AS), Producer Groups (Om.P.), Producer Organizations (OP), Urban Cooperatives, Agricultural Corporate Partnerships (A.E.S.),

d. Consortia conducting commercial activities,

e. Public and municipal enterprises and their subsidiaries, provided that:

– they have not been assigned to serve a public purpose,

– the provision of services has not been exclusively assigned to them by the state,

– their operation is not subsidized by public resources during the period of long-term obligations defined by Law 4887/22 (articles 22 & 25).

a. Creation of a new unit.

b. Expansion of the capacity of an existing unit.

c. Diversification of a unit's production into products or services never previously produced or provided, with the condition that for large enterprises, the eligible expenses exceed at least 200% of the accounting value of the assets used again, as recorded in the tax year preceding the application for inclusion of the investment plan.

d. Fundamental change of the entire production process of an existing unit.

Eligible Expenses for Regional Aid – Categories of Expenses:

a. Building Facilities. Expenses for the construction, expansion, and modernization of building facilities, including special and auxiliary installations, as well as building constructions ensuring accessibility for people with disabilities.

b. Outdoor Area Works. Earthworks, Landscaping, Fencing, Biological Treatment Facilities, Planting, Outdoor Electrical Installations, Outdoor Plumbing, Water Supply.

c. Machinery – Technical – Special Installations. Purchase and installation of modern machinery, including technical installations and general arrangements for their permanent installation and connection to the production cycle. Expenses for the construction, purchase, supply, or modernization of special installations (e.g., heating systems, air conditioning units, or storage tanks).

d. Other equipment. Expenses for the purchase and installation of other equipment or/and office furniture and utensils only if they are a basic part of the investment's productive equipment.

e. Transport Means. Any vehicles used by the company for the transportation of personnel and customers, provided that they move within the unit's premises. Vehicles with up to 6 seats are not eligible.

f. Purchase of fixed assets of a unit that ceased operation at least two years before the application submission date,

– Purchase of the unit's property (building)

– Purchase of the unit's machinery and other equipment

g. Intangible assets. Expenses for technology transfer – know-how, Product Certification, and Quality Assurance Procedures, Purchase and development of software, Business Organization Systems.

h. Payroll costs for new jobs.

The eligible expense is the payroll cost of the new jobs created as a result of the implementation of the investment plan, calculated for a period of two (2) years from the creation of each position.

Eligible Expenses Outside Regional Aid:

Aid amounts per enterprise size:

– The total aid amount per investment plan submitted by very small and small enterprises cannot exceed €3 million for all types of aid.

– The total aid amount per investment plan submitted by medium and large enterprises cannot exceed:

– €3 million for financial leasing subsidy or the subsidy of the cost of new employment creation, as well as grants in the case of aid for medium-sized enterprises in the Regional Units of Thrace.

– €5 million for tax exemption aid.

The total aid provided to each investment plan holder, including aid to associated or linked enterprises, cannot exceed a cumulative total of €20,000,000 for a single enterprise and €30,000,000 for all associated or linked enterprises.

The maximum percentage of state aid per Region and enterprise size is as follows:

| Region | Large enterprises | Medium Enterprises | Small Enterprises |

|---|---|---|---|

| Central Macedonia | 50% | 60% | 70% |

| Eastern Macedonia and Thrace | 50% | 60% | 70% |

| Western Macedonia | 40% | 50% | 60% |

| Epirus | 50% | 60% | 70% |

| Thessaly | 50% | 60% | 70% |

| Sterea Hellas | 40% | 50% | 60% |

| Ionian Islands | 40% | 50% | 60% |

| Western Greece | 50% | 60% | 70% |

| Peloponnese | 40% | 50% | 60% |

| North Aegean | 50% | 60% | 70% |

| South Aegean | 30% | 40% | 50% |

| Crete | 40% | 50% | 60% |

| Athens(Western Sector) | 15% | 25% | 35% |

| Eastern Attica, Western Attica, Piraeus, Islands | 25% | 35% | 45% |

For investment expenses in tangible fixed assets specifically for the construction, expansion, and modernization of buildings, the coefficient is set at 45%. This coefficient is set at eighty percent (80%) for investment plans implemented in buildings classified as preserved. For investment expenses in intangible assets, the coefficient is set at 50% for SMEs and 30% for large enterprises. Finally, for expenses concerning consultancy services, the coefficient is set at 50% for SMEs with a maximum limit of €50,000.

For more information, request a telephone appointment by clicking the button below, and a specialized economist from our company will contact you.

Design

Licensing

Funding

Support

Construction

Energy

Environment

Health & Safety

Cloud